Free DownloadA guide to artificial intelligence in the enterprise

This wide-ranging guide to artificial intelligence in the enterprise provides the building blocks for becoming successful business consumers of AI technologies. It starts with introductory explanations of AI's history, how AI works and the main types of AI. The importance and impact of AI is covered next, followed by information on AI's key benefits and risks, current and potential AI use cases, building a successful AI strategy, steps for implementing AI tools in the enterprise and technological breakthroughs that are driving the field forward. Throughout the guide, we include hyperlinks to TechTarget articles that provide more detail and insights on the topics discussed.

AI technologies bring operational efficiency and customer benefits to banking. Learn how GenAI and other AI tools are transforming financial services and risks to watch out for.

While artificial intelligence has gained momentum in the banking and finance sector, generative AI is taking it by storm.

The adoption of AI technologies is becoming more mainstream as financial institutions seek to automate processes, reduce operational costs and enhance overall productivity, said Sameer Gupta, North America financial services organization advanced analytics leader at EY.

Traditional machine learning (ML) techniques are widely utilized in areas such as fraud detection, loan and credit approval processes, and personalized marketing strategies, Gupta said. In fact, there are few areas where AI is not being utilized in financial services.

Now, many mature banks and financial institutions are moving to the next level with ML, natural language processing (NLP), and GenAI.

EY is seeing an increase in banks leveraging ML to streamline credit approvals, enhance fraud detection, and tailor marketing strategies, significantly improving efficiency and decision-making, he said.

In 2024, 58% of banking CIOs surveyed reported they had already deployed or are planning to deploy AI initiatives this year, according to Jasleen Kaur Sindhu, a financial services analyst at Gartner. That figure will increase to 77% in 2025, she said.

"What it says to me is the importance of AI, not just in terms of what it can do, but how fundamental it is [becoming] in terms of how a bank operates and how it creates value for its customers," Sindhu said. "In many respects, AI is becoming foundational to the success of the bank itself."

What are the top benefits of AI applications in banking?

Here are five areas where AI technologies are transforming financial operations and processes.

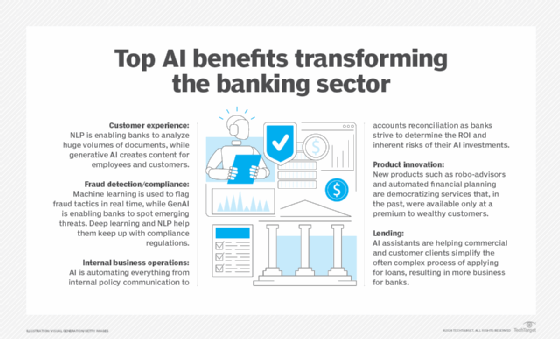

AI is transforming banking and financial services. Here is a snapshot of the benefits AI is bringing.

1. Customer experience

Natural language processing technologies are being used in banking to efficiently and accurately process and analyze large volumes of documents, Gupta said.

The development of GenAI extends NLP's ability to process language content by being able to create new content. "GenAI represents a transformative leap in innovation, particularly in content creation," he said.

EY is working with banks to deploy GenAI models designed to summarize and extract customer complaints from recorded conversations. "This is showcasing the potential of AI to improve customer service and operational insights," Gupta said.

Enabling frontline of workers is another area where GenAI is transforming how customer service is delivered, Sindhu said. Banks are increasingly giving GenAI tools to relationship managers or branch associates. This helps staff have a better understanding of the products the bank offers as well as what policies and procedures they need to follow when interacting with customers. It also provides the ability to chat or interact with data to gain a better understanding of portfolios or the customer segments they're dealing in, she said.

For many banks, chatbots are now a core component of customer service because of their ability to provide real-time responses to customer inquiries 24/7. Bank of America's Erica virtual assistant, for example, has surpassed two billion interactions and helped 42 million bank clients since its launch in June 2018.

2. Fraud detection and regulatory compliance

There is high momentum for using AI technology, including GenAI tools, for fraud detection and regulatory compliance. Machine learning can be used to analyze data in real time to look for unusual patterns and flag new fraud tactics. GenAI is used to model normal banking behavior and identify activities that deviate from the norm, enabling banks to spot emerging threats.

AI is more accurate than manual fraud detection methods or rules-based anti-fraud software, improving fraud detection processes, Sindhu said.

A core job of internal compliance teams is to comb through myriad compliance regulations. AI can complement and speed up this work, using deep learning and NLP to review compliance requirements and improve decision-making.

On the flip side, GenAI's ability to generate highly plausible, human-like communications is also making it easier and cheaper for criminals to defraud banks. GenAI could enable fraud losses to reach $40 billion in the U.S. by 2027, up from $12.3 billion in 2023, according to Deloitte's Center for Financial Services' "FSI Predictions 2024" report.

"The ready availability of new generative AI tools can make deepfake videos, fictitious voices, and fictitious documents easily and cheaply available to bad actors," the firm reported, pointing to "an entire cottage industry on the dark web that sells scamming software" ranging starting at $20. "This democratization of nefarious software is making a number of current anti-fraud tools less effective."

3. Internal business operations

GenAI is also enabling banks and financial institutions to automate internal processes as much as possible. This includes areas such as data extraction, incident resolution, or the generation of quick documents and summaries to understand internal policies and procedures -- "anything and everything that allows a bank to function day to day," Sindhu said. This will lead to productivity gains by freeing up staff to do more strategic work.

Right now, banks and financial institutions remain more focused on prioritizing internal use cases over customer-facing use cases, she added. They are trying to determine how they can manage risk and the cost-effectiveness of AI systems, how they can demonstrate ROI, and whether these investments are successful, Sindhu said. "These are the three top questions leaders are trying to work around as they scale their GenAI efforts."

4. Product innovation

Also noteworthy is the deployment of GenAI by some banks "to create game-changing use cases" through investments that allow the institution to either tap into new customer segments, create new sources of revenue, or even look at new types of business models that can be activated with the technology, Sindhu said.

For example, Erste Bank in Austria launched Financial Health Prototype, a customer-facing tool that lets banking customers ask questions about their financial life, such as how can they manage financial debt or plan for a vacation. Besides answering questions, the prototype also compares various products the bank offers that will be relevant for a specific customer.

"This is democratizing financial coaching or financial guidance" for customers, Sindhu said. Typically, these banking services are reserved for premium customers or people who can pay a fee. "But now, with GenAI, you're able to create access for all."

The bank generates ROI by acquiring new customers and improving sales leads, she said.

Deloitte's financial services report also pointed to the ability of AI tools to democratize holistic financial advice in a direct-to-consumer model by providing a more affordable proposition.

"Robo-advisory -- delivering automated advice with minimal human intervention needed -- could be a cost-effective and scalable solution to provide advice to clients who have smaller portfolios," the firm's report read, noting the ability of AI-powered robo-advisors to provide real-time, customized guidance, including portfolio selection, automatic rebalancing and tax loss harvesting. Recommendations are then delivered in "an interactive, conversational format with lower incremental client servicing costs than human advisers."

5. Lending

Customer-facing apps are also being developed, especially in the lending space. For example, U.S.-based Bankwell Bank has deployed Cascading AI's Casca conversational AI assistant loan origination system for small business owners.

The assistant answers borrowers' questions about often complex lending products and provides additional information or documents small business owners need to be able to apply for a loan. They can upload an application, and the assistant also regularly reaches out if the small business owner abandons the application midway.

"It is improving the process of creating more transparency … for small business owners to quickly access financial help through the bank via the assistant," Sindhu said. After introducing the assistant, the quality of sales leads were four to five times higher than those from organic modeling, according to Sindhu.

What are the risks and challenges of using AI in banking?

Concerns about AI haven't been alleviated much in the past few years, indicating that more protections need to be implemented to give users confidence about deploying systems.

Data privacy

Because AI technologies are still evolving, it is inevitable that along with the benefits they deliver also come risks. An overarching issue is privacy. AI can extract personal information from sources including emails, social media posts, and images without someone realizing their data is being collected and analyzed. This could potentially lead to misuse of sensitive, personally identifiable information without consent.

Data privacy, security risks and transparency ranked high on the list of the AI issues that board members are digging into, according to a report from EY. "Generative AI has amplified these concerns," the report read.

Issues about data privacy also come into play when the question of publicly available systems respect user input data privacy, and whether there is a risk of data leakage, noted the European Central Bank.

Bias, AI ethics and fairness

Concerns about AI ethics, fairness and bias; trust in AI models; and AI benefits and value estimations remain the top three barriers to its implementation, Sindhu said.

In many respects, AI is becoming foundational to the success of the bank itself.

Jasleen Kaur SindhuFinancial services analyst, Gartner

Additionally, board oversight can be complicated by a lack of clear regulatory direction, according to EY data. Regulators have expressed concern about embedded bias in algorithms used to make credit decisions and chatbots sharing inaccurate information, the firm said.

"Algorithmic bias is a major concern as AI systems can perpetuate existing biases from training data. This can lead to unfair treatment in loan approvals, credit scoring or fraud detection," Sindhu said. "Similarly, lack of transparency and explainability in many AI models complicates regulatory compliance and may erode customer trust."

As AI systems become more advanced and autonomous, such as with GenAI, which can easily create convincing and potentially harmful content, banks are frontloading their AI governance efforts to ensure new AI risks are considered and managed appropriately, Sindhu said.

To address these challenges, banks are also investing in robust AI governance frameworks, continuous monitoring and auditing, stakeholder engagement, and adherence to ethical guidelines and regulatory standards, she said.

Future trends and predictions

AI is poised to transform banking with personalized services and tailored financial products, enhancing customer interactions, Gupta said. "Strengthening regulations and security for AI will boost trust and investment, integrating AI across functions like customer service, risk management and fraud detection [as well as] redefining the industry's operations and competition."

GenAI is also expected to have a significant impact on productivity across financial services. Deloitte predicts that the top 14 global investment banks can boost their front-office productivity by as much as 27% to 35% with GenAI. This would result in additional revenue of $3.5 million per front-office employee by 2026, the firm said.

Esther Shein is a veteran freelance writer specializing in technology and business. A former senior writer at eWeek, she writes news, features, case studies and custom content.